How Right-of-Use Assets and Lease Liabilities Work (ASC 842, IFRS 16, GASB 87)

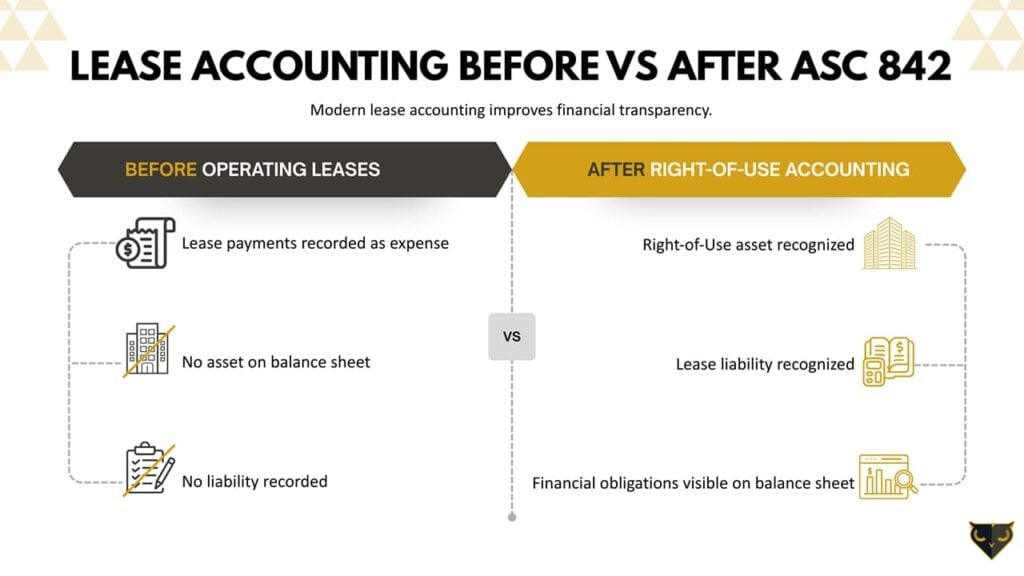

A right-of-use (ROU) asset is the right to use a leased asset over the lease term. Together with the matching lease liability, the present value of future payments owed – it represents the foundation of modern lease accounting under ASC 842, IFRS 16, and GASB 87. Before these standards, almost every operating lease lived in the footnotes; today, almost every lease lives on the balance sheet.

This guide explains what an ROU asset is, what it includes, how to calculate it step by step, and how the three major lease accounting standards differ in their treatment. It includes a complete worked example with real numbers and shows how lease accounting software automates the entire workflow.

Quick definition: A right-of-use asset is the lessee’s recognition of the economic benefits of using a leased asset for the lease term. It is recorded on the balance sheet at lease commencement and amortized over tthe lease term — or, for finance leases and IFRS 16, over the shorter of the lease term or the asset’s useful life.

Right-of-Use Asset vs Lease Liability

|

Concept |

Definition |

|---|---|

|

Right-of-Use Asset |

The right to use a leased asset over the lease term |

|

Lease Liability |

The present value of future lease payments owed |

These two elements form the foundation of modern lease accounting under ASC 842, IFRS 16, and GASB 87.

Key takeaways

- The ROU asset and the lease liability are recorded together at lease commencement, both measured at the present value of future lease payments.

- The ROU asset is then adjusted for prepaid rent, initial direct costs, and lease incentives – so it rarely equals the lease liability exactly.

- ASC 842 keeps two lease classifications (operating, finance); IFRS 16 uses a single model; GASB 87 applies a single model for government entities.

- The ROU asset is amortized differently depending on classification: straight-line for finance/IFRS 16, plug-balanced for ASC 842 operating.

- Lease accounting software calculates ROU at commencement, every period, and through every modification automatically.

What is a Right-of-Use (ROU) Asset?

A right-of-use asset represents a lessee’s right to control the use of an identified asset for the lease term in exchange for consideration. In plain English, it’s the accounting recognition that you have economic value tied up in something you’re leasing – even though you don’t own it.

Before ASC 842 and IFRS 16, lessees recognized operating leases as a simple periodic expense and disclosed future commitments only in the notes. The result: trillions of dollars in lease obligations sat off the balance sheet, hidden from investors and analysts. The new standards force those obligations onto the books as ROU assets and lease liabilities, giving stakeholders a much more complete view of the company’s financial position.

What is a Lease Liability?

The lease liability is the financial obligation the lessee owes the lessor under the lease – measured at the present value of future lease payments, discounted at the rate implicit in the lease (or the lessee’s incremental borrowing rate, IBR, when the implicit rate is not readily determinable).

The lease liability and the ROU asset are recorded together at commencement and start at similar values. From that point on, they diverge: the liability is reduced through lease payments using the effective-interest method, while the ROU asset is amortized over the lease term according to its classification.

How to Calculate the Right-of-Use Asset (Step by Step)

The ROU asset starts from the lease liability – the present value of future lease payments – and is then adjusted for cash flows that occurred at or before commencement:

- Plus: prepaid lease payments made before commencement

- Plus: initial direct costs incurred to obtain the lease (e.g., broker commissions)

- Less: lease incentives received from the lessor

Example

Imagine your company signs a 5-year office lease with the following terms:

- Annual lease payment: $100,000, payable at the end of each year

- Lease term: 5 years

- Incremental borrowing rate (IBR): 5%

- Prepaid rent: $20,000 (paid at commencement)

- Initial direct costs: $5,000 (broker commission)

- Lease incentive: $10,000 (tenant improvement allowance from landlord)

Step 1 – Compute the lease liability:

The present value (PV) of five annual payments of $100,000 each, discounted at a rate of 5%, is $432,948.

Step 2 – Adjust to arrive at the ROU asset:

- Lease liability: $432,948

- Plus prepaid rent: + $20,000

- Plus initial direct costs: + $5,000

- Less lease incentive: − $10,000

- ROU asset at commencement: $447,948

The initial journal entry recognizes both the ROU asset and the lease liability:

|

Account |

Debit |

Credit |

|

Right-of-Use Asset |

$447,948 |

|

|

Lease Liability |

$432,948 |

|

|

Cash (prepaid rent + initial direct costs − incentive) |

$15,000 |

To record the ROU asset, lease liability, and net cash flows at lease commencement.

Notice that the ROU asset ($447,948) is larger than the lease liability ($432,948). They start with the same PV-of-payments base, but adjustments for prepaid rent and initial direct costs lift the asset above the liability. They are NOT supposed to match.

ROU Asset and Lease Liability Under ASC 842

ASC 842 keeps two lessee classifications – operating and finance – that produce identical balance sheet recognition but different income statement profiles.

For an operating lease, the income statement shows a single, straight-line lease expense over the lease term. The ROU asset is amortized on a plug-balance basis: each period’s amortization equals the straight-line lease expense minus the period’s interest, so total lease expense remains flat.

For a finance lease, expense is split into interest (effective-interest method on the liability) and amortization (straight-line on the ROU asset). This results in front-loaded total expense – higher in early years, lower later – and a positive impact on EBITDA because both interest and amortization are excluded from EBITDA.

ROU Asset and Lease Liability Under IFRS 16

IFRS 16 eliminates the operating-lease classification for lessees. With limited exceptions for short-term and low-value leases, every lease is treated like an ASC 842 finance lease: ROU asset depreciated straight-line, lease liability amortized using the effective-interest method, and expense split into depreciation plus interest on the income statement.

Two practical exemptions reduce the operational burden:

- Short-term leases: leases with a term of 12 months or less, no purchase option reasonably certain to be exercised.

- Low-value leases: leases of underlying assets that are low in value when new

- The IASB referenced approximately $5,000 USD as informal guidance during standard-setting, though no hard threshold is specified in IFRS 16 itself – laptops and office furniture are common examples).

ROU Asset and Lease Liability Under GASB 87

GASB 87 applies to state and local government entities in the United States. Like IFRS 16, it uses a single recognition model – every qualifying lease produces an intangible right-to-use asset (the GASB equivalent of an ROU asset) and a lease liability.

Key differences from ASC 842 and IFRS 16:

- GASB 87 explicitly treats the ROU as an intangible asset rather than the broader balance sheet line used in ASC 842/IFRS 16.

- GASB 87 requires the lessee’s incremental borrowing rate unless the rate implicit in the lease is readily determinable. In practice, many government entities derive this rate from their general obligation or revenue bond yields as a proxy for their incremental borrowing rate.

- Disclosures align with the broader GASB government reporting framework.

Standards Comparison Table

|

Feature |

ASC 842 |

IFRS 16 |

GASB 87 |

|---|---|---|---|

|

Operating leases |

Yes (separate classification) |

No |

No |

|

Finance / single model |

Yes |

Yes |

Yes |

|

Balance sheet recognition |

Yes |

Yes |

Yes |

|

Short-term lease exemption |

Yes (≤12 mo) |

Yes (≤12 mo) |

Yes |

|

Low-value exemption |

No |

Yes |

No |

|

Discount rate |

IBR (or risk-free for private) |

IBR |

Government-specific rate |

Calculating ROU assets manually for hundreds of leases – across multiple standards, currencies, and modifications – is error-prone and audit-risky. Black Owl handles it automatically: ROU recognition, amortization, modifications, and disclosures across ASC 842, IFRS 16, and GASB 87 in one platform. Book a 10-minute demo →

How ROU Assets Impact Financial Statements

Balance sheet

Total assets and total liabilities both increase at lease commencement by roughly the same amount (the ROU asset and lease liability). Investors and analysts will see a meaningfully larger balance sheet for the same operating activity – particularly noticeable for retail, real estate, and airline operators with significant lease portfolios.

Income statement

Under ASC 842 operating leases, total lease expense is flat over the lease term (straight-line). Under finance leases and IFRS 16, expense is front-loaded – higher in early years, lower later. EBITDA improves under finance/IFRS 16 because both interest and amortization sit below the EBITDA line.

Cash flow statement

Under IFRS 16 and ASC 842 finance leases, principal payments are classified as financing activities. Interest payments under ASC 842 finance leases follow the entity’s existing accounting policy election under ASC 230 — either operating or financing activities. Under ASC 842 operating leases, the entire payment is presented in operating activities.

Key ratios

- Debt-to-equity: rises as lease liabilities are recognized.

- Asset turnover: declines because total assets grow.

- EBITDA: rises (often materially) for finance leases and IFRS 16 leases.

- Interest coverage: falls because lease interest is now recognized.

Common Mistakes in ROU Asset Accounting

1. Treating the ROU asset and lease liability as identical

They start similar but diverge from day one. The ROU is adjusted for prepaid rent, initial direct costs, and incentives at commencement, and follows a different amortization pattern over the lease term. Treating them as equal in spreadsheets creates audit issues immediately.

2. Forgetting to remeasure the ROU after lease modifications

Term extensions, scope changes, and significant payment changes trigger a remeasurement of the lease liability – and a corresponding adjustment to the ROU asset. Many spreadsheet-based teams update the liability and forget the ROU side, leaving the books carrying inconsistent balances.

3. Inconsistent IBR application across the portfolio

The IBR drives the entire ROU and liability valuation. Applying different IBR methodologies across leases creates a comparability problem your auditor will flag. Document the IBR policy once and apply it consistently.

4. Missing embedded leases

Many service contracts, IT outsourcing agreements, and supply arrangements contain embedded leases that need ROU recognition. Limiting your ROU analysis to contracts explicitly labeled “lease” will leave material obligations off the balance sheet.

How Software Automates ROU Asset Accounting

Calculating ROU manually for ten leases is tedious. For a hundred leases – with adjustments, modifications, multi-currency conversions, and three reporting standards – it’s functionally impossible to do without errors.

Lease accounting software like Black Owl Systems handles the entire workflow:

- Calculates ROU asset and lease liability at commencement, including all adjustments (prepaid rent, IDC, incentives).

- Maintains period-by-period ROU and liability balances under ASC 842, IFRS 16, and GASB 87 in parallel.

- Auto-remeasures the ROU through every modification and reassessment.

- Generates compliant journal entries and posts them directly to your ERP.

- Produces audit-ready disclosures and roll-forward schedules.

See it in action: book a 10-minute demo and walk through how Black Owl computes ROU assets – for your actual leases. No prep work required.

Frequently Asked Questions

What is included in the right-of-use asset?

The ROU asset includes the present value of future lease payments (which equals the initial lease liability), plus any prepaid rent and initial direct costs, less any lease incentives received from the lessor.

How is the lease liability different from the ROU asset?

The lease liability is the financial obligation – present value of payments owed. The ROU asset is the economic right to use the asset. They start with the same base value but diverge over time as the asset is amortized and the liability is reduced through payments.

Do all three standards (ASC 842, IFRS 16, GASB 87) treat ROU assets the same way?

All three require ROU asset recognition on the balance sheet, but ASC 842 keeps a separate operating-lease classification, IFRS 16 treats almost all leases under a single finance-like model, and GASB 87 applies its own single model for government entities.

How is the ROU asset amortized?

Under ASC 842 finance leases and under IFRS 16, the ROU asset is amortized straight-line over the shorter of the lease term or the asset’s useful life. Under ASC 842 operating leases, the ROU amortization is plug-balanced so that total lease expense remains straight-line.

Where does the ROU asset appear on the balance sheet?

ROU assets typically appear as a separate line item under non-current assets, sometimes grouped with property, plant, and equipment. Companies disclose ROU assets by underlying asset class (real estate, equipment, vehicles) in the notes.

Can lease accounting software calculate ROU assets automatically?

Yes. Platforms like Black Owl Systems compute the ROU asset, lease liability, amortization schedule, and journal entries from the lease contract data – across ASC 842, IFRS 16, and GASB 87 – and post entries directly to any ERP.

Bringing it all together

ROU assets transformed lease accounting from a simple footnote disclosure into a balance sheet line item that affects total assets, total liabilities, EBITDA, and key financial ratios. The math is straightforward at the single-lease level, but the operational discipline of doing it correctly every period across an entire portfolio is where teams lose time and risk audit findings.

If your team is managing ROU assets in spreadsheets across more than a handful of leases, the question is not whether errors are happening, it is whether they surface before or during the audit.

The next step is simple: see how Black Owl handles it for organizations with anywhere from 5 to 5,000 leases. See a demo of Black Owl in less than 30 minutes.nd we use your actual lease data.

Related resources

Greg Kautz

http://blackowlsystems.comGreg Kautz, CPA, CMA is a seasoned management consultant and professional accountant with over 40 years of experience in the consulting and energy sectors. At Black Owl Systems, Greg brings deep expertise in ERP systems, corporate finance, strategic planning, and technology integration.