Understanding Finance Lease vs Operating Lease: A Comprehensive Overview

A finance lease transfers the risks and rewards of ownership to the lessee, while an operating lease grants temporary use without ownership transfer. Under ASC 842, both lease types must be recognized on the balance sheet – but the income statement profile, the EBITDA impact, and the classification criteria differ significantly. Getting the classification right at lease commencement matters: misclassification flips the financial reporting story for the entire lease term.

This guide explains the 5-criteria ASC 842 classification test, walks through the differences in journal entries and financial statements, compares EBITDA outcomes, and shows how lease accounting software automates the classification at scale. A free classification checklist is included at the end.

Quick definition: Under ASC 842, a lease is classified as a finance lease if it meets any of five criteria related to ownership transfer, purchase option, asset use, lease term, or payment value. If none of these are met, the lease is classified as operating.

Key takeaways

- Both lease types appear on the balance sheet under ASC 842 (ROU asset + lease liability).

- Finance leases split expense into interest + amortization, both excluded from EBITDA – increasing EBITDA.

- Operating leases recognize a single straight-line lease expense – neutral EBITDA impact (similar to old ASC 840).

- Classification is determined at commencement using the ASC 842 5-criteria test. Meeting any one criterion = finance lease.

- IFRS 16 eliminates this distinction entirely – almost all leases are treated like ASC 842 finance leases.

Finance Lease vs Operating Lease – Quick Answer

The fastest way to internalize the difference is by what each lease tries to economically replicate:

- A finance lease is essentially a financed purchase. The lessee uses the asset for most of its economic life and absorbs most of the risk and reward of ownership – even though legal title may not transfer.

- An operating lease is essentially a rental. The lessee uses the asset for a portion of its life and the lessor retains the risks and rewards of ownership.

Under ASC 842 both types now appear on the balance sheet, but the income statement, classification rules, and EBITDA impact diverge.

What is a Finance Lease?

A finance lease (called a “capital lease” under the legacy ASC 840 standard) is a lease that transfers substantially all the risks and rewards of ownership to the lessee. The lessee accounts for the leased asset much like a financed purchase: an asset on the balance sheet, a liability for the financing, separate depreciation and interest expense on the income statement.

Distinguishing Finance Leases

ASC 842 provides specific criteria to distinguish finance leases from operating leases. The classification test is performed at lease commencement, and the result drives the entire subsequent accounting profile.

How to Classify a Lease Under ASC 842

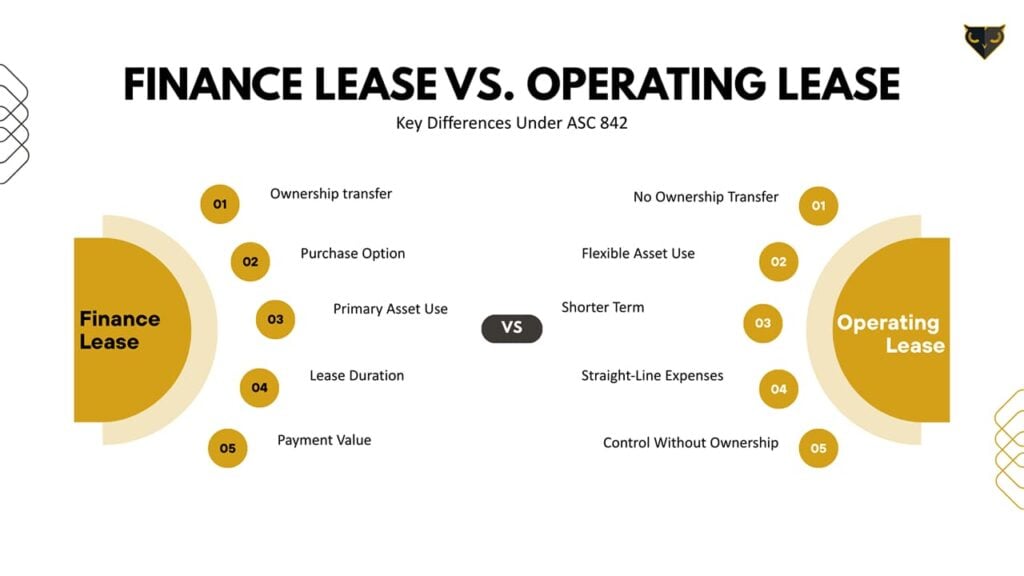

To determine whether a lease is classified as a finance lease or operating lease under ASC 842, organizations should evaluate the lease against five key criteria:

- Does ownership transfer at the end of the lease?

- Is there a purchase option that is reasonably certain to be exercised?

- Does the asset have no alternative use to the lessor?

- Does the lease term represent a major part of the asset’s economic life?

- Do lease payments represent substantially all of the asset’s fair value?

If any one of these criteria is met, the lease is classified as a finance lease. If none are met, it is classified as an operating lease.

FASB intentionally avoided bright-line numerical thresholds in ASC 842 (unlike the old ASC 840, which used 75%/90% rules). Most companies still apply 75% and 90% as practical guidance – but the standard requires judgment, and your auditor will want documented reasoning when leases approach the boundary.

What is an Operating Lease?

An operating lease is a lease that does not meet any of the five finance lease criteria. The lessee uses the asset for a portion of its economic life, and the lessor retains the risks and rewards of ownership. Common examples: short-term office space leases, equipment rentals, vehicle leases for moderate periods.

Under ASC 842, operating leases still result in a balance sheet presence (ROU asset + lease liability), which is the major change from ASC 840. But on the income statement, an operating lease produces a single straight-line lease expense – preserving the smooth expense pattern that finance professionals were used to under the old standard.

Side-by-Side Comparison

|

Topic |

Finance Lease |

Operating Lease |

|---|---|---|

|

Balance sheet |

ROU asset + lease liability |

ROU asset + lease liability |

|

Income statement |

Interest + Amortization (separate lines) |

Single lease expense (straight-line) |

|

Expense pattern |

Front-loaded (higher early years) |

Straight-line over lease term |

|

EBITDA impact |

Increases EBITDA |

Reduces EBITDA (similar to ASC 840) |

|

Cash flow statement |

Interest in operating, principal in financing |

Entire payment in operating |

|

IFRS 16 equivalent |

All IFRS 16 leases follow this model |

No IFRS 16 equivalent for lessees |

Income Statement and Balance Sheet Impact

The classification choice has real consequences for reported earnings and key financial ratios. Consider a 5-year lease with $100,000 annual payments at a 5% IBR:

Year 1 expense comparison

- Finance lease: Interest $21,647 + Amortization $86,590 = $108,237 total expense.

- Operating lease: Single lease expense of $100,000 (straight-line).

Year 5 expense comparison

- Finance lease: Interest $4,762 + Amortization $86,590 = $91,352 total expense.

- Operating lease: Single lease expense of $100,000 (still straight-line).

Two takeaways: finance leases are front-loaded (higher cost early, lower cost later); operating leases are flat. Across the full 5 years, total expense is $500,000 for both – but the timing differs significantly, and the EBITDA presentation differs every single period.

EBITDA: The Hidden Reason Classification Matters

Because EBITDA explicitly excludes interest and depreciation/amortization, finance lease expense is excluded from EBITDA – while operating lease expense is fully included. The result: a finance lease classification can artificially boost EBITDA by tens or hundreds of millions of dollars for asset-heavy industries.

This matters for:

- EBITDA-based debt covenants – classification can affect compliance.

- Performance reporting to investors and analysts.

- Internal compensation tied to EBITDA targets.

- M&A valuations using EBITDA multiples.

Managing lease classification and compliance under ASC 842 can quickly become complex at scale – especially when EBITDA covenants are at stake. See how Black Owl Systems automates lease accounting, classification, and reporting

Common Mistakes in Lease Classification

1. Defaulting to operating lease classification

Many teams treat operating as the default and only flag finance leases when ownership clearly transfers. This misses the “major part of economic life” and “substantially all fair value” criteria, which can capture leases that don’t look like financed purchases at first glance.

2. Failing to document the classification analysis

Auditors will ask for the classification analysis at lease commencement, especially for borderline cases. A documented analysis showing the 5 criteria and the conclusion is much easier than reconstructing the reasoning a year later.

3. Forgetting to reassess after a modification

Lease modifications can change classification. A lease term extension that pushes the term beyond a “major part of economic life” can convert an operating lease into a finance lease – and require remeasurement and reclassification.

4. Inconsistent application across the portfolio

Different teams using different criteria thresholds creates an audit problem. Document the company’s classification policy (including how 75% / 90% thresholds are interpreted) and apply it consistently across every lease.

How Software Automates Lease Classification

For a single lease, the 5-criteria test is a 15-minute exercise. For a portfolio of 100+ leases, with periodic modifications and reassessments, manual classification becomes a permanent maintenance burden – and a recurring source of audit findings.

Lease accounting software like Black Owl Systems handles classification automatically:

- Captures lease terms and runs the 5-criteria test at commencement.

- Documents the classification analysis with full audit trail.

- Flags leases for reclassification when modifications change the criteria results.

- Generates the right journal entries (operating vs finance) automatically based on classification.

- Reports portfolio classification mix for management visibility.

See it in action: book a 10-minute demo and walk through how Black Owl classifies leases against the ASC 842 criteria – for your actual portfolio.

Frequently Asked Questions

What is the difference between a finance lease and an operating lease?

A finance lease transfers ownership-like risks and benefits to the lessee, while an operating lease provides temporary use without transferring ownership. Under ASC 842, both types appear on the balance sheet as ROU asset + lease liability, but income statement presentation and EBITDA impact differ.

Do both lease types appear on the balance sheet under ASC 842?

Yes. Both finance and operating leases require recognition of a right-of-use asset and lease liability – this is the most significant change from ASC 840, which kept operating leases off the balance sheet.

How do you classify a lease under ASC 842?

A lease is classified as a finance lease if it meets any of five criteria: ownership transfer at end of term, purchase option reasonably certain to be exercised, no alternative use to the lessor, lease term covering a major part of the asset’s economic life, or payments representing substantially all of the asset’s fair value. If none are met, it is operating.

Why does expense recognition differ between lease types?

Finance leases separate interest and amortization (front-loaded total expense). Operating leases use a straight-line single-expense approach. The result is identical total expense over the lease term, but very different period-by-period income statement profiles.

Does the same classification apply under IFRS 16?

No. IFRS 16 eliminates the distinction for lessees – almost all leases are treated like ASC 842 finance leases on the balance sheet and income statement. Lessor accounting under IFRS 16 still uses classification, but the lessee model is a single approach.

Conclusion

Lease classification under ASC 842 isn’t just an academic exercise. It determines income statement presentation, EBITDA impact, debt covenant compliance, and how investors interpret your operating performance. Getting it right at commencement, documenting the analysis, and reassessing through modifications are the table stakes for clean ASC 842 compliance.

If your team is classifying leases manually in spreadsheets, the next step is short: see how Black Owl handles the 5-criteria test at scale, generates the right journal entries based on classification, and produces audit-ready documentation for every lease. The demo is 10 minutes.

Managing lease classification and compliance under ASC 842 can quickly become complex at scale. See how Black Owl Systems automates lease accounting, classification, and reporting →

Related resources

Greg Kautz

http://blackowlsystems.comGreg Kautz, CPA, CMA is a seasoned management consultant and professional accountant with over 40 years of experience in the consulting and energy sectors. At Black Owl Systems, Greg brings deep expertise in ERP systems, corporate finance, strategic planning, and technology integration.