Black Owl simplifies your lease accounting software with a robust, user-friendly ASPE solution. Changes to ASPE standards can be difficult to track, but our software keeps both lessees and lessors compliant with Section 3065 of the handbook.

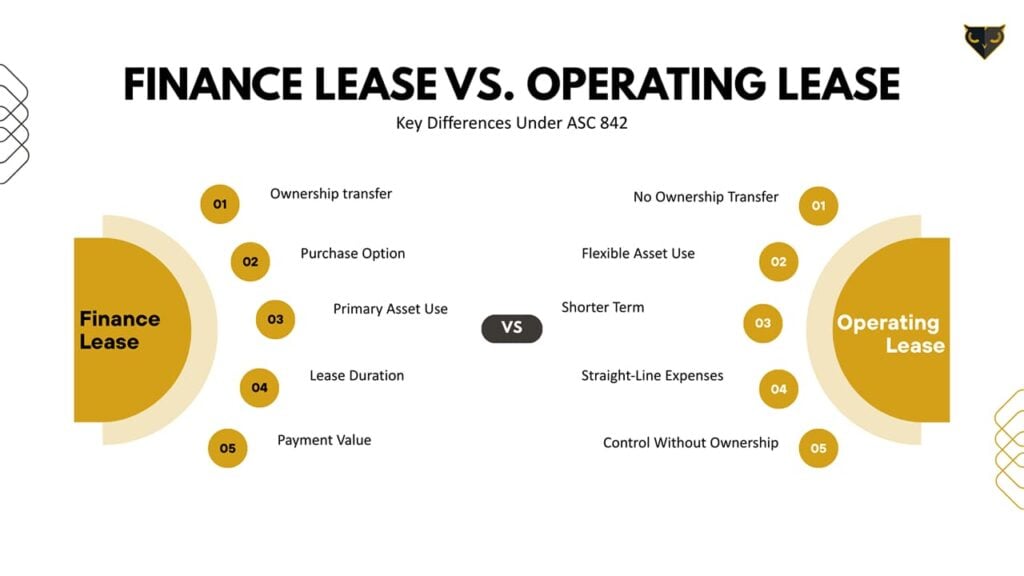

Operating leases don’t transfer substantially all the benefits and risks of ownership. The lessee records the lease payments as an expense on a straight-line basis over the lease term.

A capital lease, under ASPE 3065, is when substantially all risks and benefits of ownership are transferred to the lessee. It is recognized as an asset and liability by the lessee.

Black Owl's system provides complete disclosure reports that meet accounting standards and comply with lease disclosure requirements.

Customizable Lease Hub

Create and save ad-hoc reports based on unique fields. Create reports of upcoming and past critical dates. Easy to copy and paste into Excel.

Lease Entry

User Friendly

Black Owl’s lease entry is designed to be user-friendly, with a simple interface and intuitive navigation, making it easy to input and manage lease data in minutes.

Effortlessly make lease modifications and reassessments into a streamlined process, enhancing efficiency, reducing errors, and improving overall lease management.

Retroactive Adjustments

Manage lease changes with ease for both current and retroactive periods maintaining strong audit trails.

The primary difference between ASPE and IFRS is how they classify and record leases. ASPE distinguishes between capital and operating leases. However, IFRS classifies most leases as ‘right-of-use’ assets, which means both types are effectively accounted for as capital leases under ASPE.

Recording a Lease

For capital leases, lessees record an asset and a liability at the present value of the minimum lease payments. For operating leases, lessees account for the lease payments as an expense.

ASPE 3065 has undergone several amendments to address issues such as:

Lease modifications and rent concessions due to unforeseen circumstances.

Providing clarity on determining the lease term, which may include periods covered by options to extend or terminate the lease.

Guidance on accounting treatment for initial direct costs.

These changes aim to provide relief and address the possible assurance implications for private enterprises.

FAQ

Frequently Asked Questions

What is ASPE lease accounting?

ASPE lease accounting refers to the accounting treatment of leases as outlined by the Accounting Standards for Private Enterprises (ASPE) in Canada. It categorizes leases into capital and operating leases, each having different accounting treatments.

What is the difference between a capital lease and an operating lease under ASPE?

A capital lease transfers substantially all the risks and benefits of ownership from the lessor to the lessee. An operating lease, on the other hand, does not significantly transfer the benefits and risks associated with ownership.

What is a lease term under ASPE lease accounting?

A lease term under ASPE lease accounting is the non-cancellable period for which the lessee has contracted to lease the asset together with any further terms for which the lessee has the option to continue the lease.

How are lease modifications treated under ASPE lease accounting?

Lease modifications under ASPE lease accounting are usually treated as new leases from the date of modification. However, minor modifications are typically accounted for as a change in accounting estimates.

What are the financial statement disclosure requirements for ASPE lease accounting?

ASPE lease accounting requires disclosures related to the nature and extent of leases, including a general description of significant leasing arrangements, future minimum lease payments, total contingent rents, and lease and sublease income.

ASPE 3065

ASPE 3065 Lease Accounting Software Features

Variable Costs

Variable cost lease agreements can be tracked and units consumed updated in our easy to use month-end close step.

Sublease

Easily create and track sublease agreements, including multiple levels of subleases.

Mass UpLoads

Mass load template with built-in validations for master data and lease information.

Data security

Black Owl's system provides world-class enterprise security measures to ensure that lease accounting data is protected.

Learn How BlackOwl Has Helped 100+ Teams Elevate Their Systems

Let's have a chat

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.