Lease Accounting Journal Entries (2026): Complete ASC 842 & IFRS 16 Guide with Examples

Key takeaways

- Both ASC 842 and IFRS 16 require lessees to record an ROU asset and lease liability at lease commencement.

- ASC 842 keeps two lessee classifications (operating and finance) with different income statement profiles. IFRS 16 uses a single model where almost all leases are treated like ASC 842 finance leases.

- Each subsequent period needs entries for interest, amortization (or straight-line lease expense), and the cash payment.

- Lease modifications and reassessments require remeasurement of the liability and a corresponding adjustment to the ROU asset.

- Lease accounting software automates these entries, posts them to any ERP, and produces the audit trail required by Big 4 auditors.

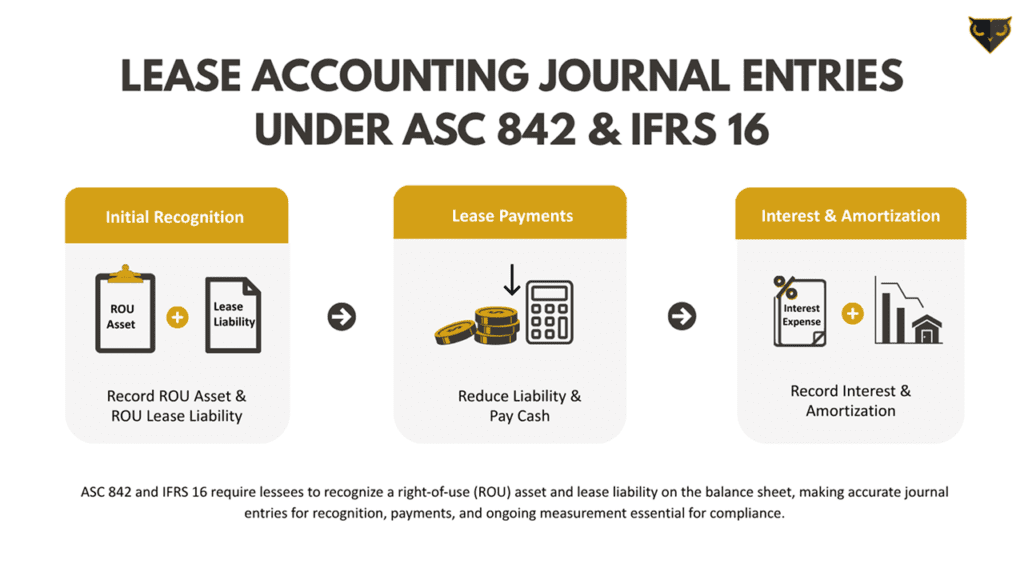

What Are Lease Accounting Journal Entries?

A lease accounting journal entry is the bookkeeping record that captures every accounting consequence of a lease – at lease commencement, every reporting period through the end of the lease term, and at any modification, reassessment, or termination event in between.

Where one rent-expense entry used to suffice, lessees now need an initial recognition entry, an interest entry, an amortization entry, a payment entry, and frequently remeasurement entries – each with rules that differ between ASC 842 and IFRS 16.

Initial Recognition: Recording the ROU Asset and Lease Liability

At lease commencement (the date the lessor makes the asset available for use), the lessee must recognize a right-of-use asset and a corresponding lease liability. Both are measured at the present value of future lease payments, discounted at the rate implicit in the lease or when that rate is not readily determinable, the lessee’s incremental borrowing rate (IBR).

The ROU asset is then adjusted for prepaid rent, initial direct costs, and any lease incentives received. To keep the worked examples below clean, we will assume those adjustments are zero.

The worked example used throughout this guide

Imagine your company signs a 5-year office lease with the following terms:

- Annual lease payment: $100,000, payable at the end of each year

- Lease term: 5 years

- Incremental borrowing rate (IBR): 5%

- No prepaid rent, no initial direct costs, no lease incentives

The present value of five annual payments of $100,000 discounted at 5% is $432,948. This is the value at which both the ROU asset and the lease liability are initially recorded.

Lease classification: Operating lease under ASC 842 (none of the five finance lease criteria are met); capitalized lease under IFRS 16

ASC 842 – Initial Entry (Operating Lease)

Under ASC 842, an operating lease still requires balance sheet recognition. The initial entry is identical for operating and finance leases:

|

Account |

Debit |

Credit |

|

Right-of-Use Asset |

$432,948 |

|

|

ROU Lease Liability |

$432,948 |

To record the right-of-use asset and lease liability at lease commencement (5-year office lease, $100,000 annual payment, 5% IBR).

ASC 842 – Initial Entry (Finance Lease)

Same entry as the operating lease. The classification only matters from the second journal entry forward – at initial recognition, ASC 842 treats both lease types identically.

|

Account |

Debit |

Credit |

|

Right-of-Use Asset |

$432,948 |

|

|

ROU Lease Liability |

$432,948 |

IFRS 16 – Initial Entry (All Capitalized Leases)

IFRS 16 eliminates the operating-lease classification for lessees almost entirely. Every lease that does not qualify for the short-term or low-value exemption is recognized in the same way:

|

Account |

Debit |

Credit |

|

Right-of-Use Asset |

$432,948 |

|

|

ROU Lease Liability |

$432,948 |

Initial recognition is identical across all three scenarios. The classification only changes how you record subsequent entries – interest, amortization, and the income-statement presentation.

How to Determine Lease Classification Under ASC 842

Before you can record the right entries, you need to know what type of lease you have. Under ASC 842, a lessee must run a five-criteria classification test at lease commencement. If any one of the following applies, the lease is a finance lease:

- Ownership transfers to the lessee by the end of the lease term

- The lessee has a purchase option and is reasonably certain to exercise it

- The lease term covers the major part of the remaining economic life of the asset (the threshold used in practice is generally 75% or more)

- The present value of lease payments equals or exceeds substantially all of the fair value of the asset (the threshold used in practice is generally 90% or more)

- The underlying asset is so specialized it has no alternative use to the lessor at the end of the lease term

If none of the five criteria are met, the lease is an operating lease. This classification decision is made once, at commencement, and it drives the entire subsequent journal entry pattern, which is why getting it documented properly matters. Auditors will ask.

|

IFRS 16 NOTE Under IFRS 16, lessees do not run this classification test. Almost every lease is treated like an ASC 842 finance lease, with the only exemptions being short-term leases (12 months or less) and leases of low-value assets. |

Monthly Lease Payment Entries

Although the worked example uses annual payments for clarity, real-world leases pay monthly. The monthly journal entry has the same components – interest accrual, principal reduction (liability paydown), and ROU asset amortization – but the math is computed at a monthly rate.

To stay readable, the rest of this guide works in annual figures. The principles, schemas, and entries are identical for monthly accounting; you simply use the monthly periodic rate (annual rate ÷ 12) and apply payments month by month.

Year 1 amortization figures

Before recording the year-end entries, calculate the interest and principal split for Year 1:

- Beginning lease liability: $432,948

- Interest for Year 1 = $432,948 × 5% = $21,647

- Cash payment = $100,000

- Principal reduction = $100,000 − $21,647 = $78,353

- Ending lease liability = $432,948 − $78,353 = $354,595

Interest Expense and Amortization

This is where ASC 842 and IFRS 16 diverge. The interest calculation is the same – apply the discount rate to the carrying liability – but how the ROU asset is amortized, and how the income statement presents the cost, depends on the classification.

ASC 842 – Operating Lease (Year 1 entries)

Under an operating lease, the income statement shows a single, straight-line lease expense over the lease term. Total lease cost across all five years is $500,000 ($100,000 × 5), so the straight-line annual lease expense is $100,000.

To make the income statement straight-line while still tracking the liability with the effective-interest method, the ROU amortization is plug-balanced: it equals the straight-line lease expense minus the period’s interest. In Year 1, that’s $100,000 − $21,647 = $78,353.

The composite Year 1 entry:

|

Account |

Debit |

Credit |

|

Lease Expense |

$100,000 |

|

|

Cash |

$100,000 |

|

|

Lease Liability |

$78,353 |

|

|

Right-of-Use Asset (amortization) |

$78,353 |

To record straight-line lease expense, the cash payment, and the corresponding reductions in the lease liability and ROU asset for Year 1 (operating lease, ASC 842).

ASC 842 – Finance Lease (Year 1 entries)

Under a finance lease, expense is split into two distinct lines: interest expense and amortization expense. Interest follows the effective-interest method (already calculated: $21,647). Amortization is typically straight-line over the shorter of the lease term or the asset’s useful life – here, $432,948 ÷ 5 years = $86,590.

Year 1 entries:

|

Account |

Debit |

Credit |

|

Interest Expense |

$21,647 |

|

|

Lease Liability |

$78,353 |

|

|

Cash |

$100,000 |

To record interest expense, principal reduction, and the cash payment for Year 1 (finance lease, ASC 842).

|

Account |

Debit |

Credit |

|

Amortization Expense – ROU Asset |

$86,590 |

|

|

Accumulated Amortization – ROU Asset |

$86,590 |

To record straight-line amortization of the ROU asset for Year 1 (finance lease, ASC 842).

Notice the front-loaded cost pattern of a finance lease: total Year 1 expense is $21,647 + $86,590 = $108,237, versus the flat $100,000 under operating-lease treatment. As the liability shrinks, interest declines and total expense falls to less than $100,000 in later years.

IFRS 16 – Year 1 entries (single model)

Under IFRS 16, the entries are identical to the ASC 842 finance lease above. Every capitalized lease produces interest expense plus amortization, with no straight-line plug-balanced operating-lease alternative.

ASC 842 vs IFRS 16: Journal Entry Differences

Initial recognition is identical. The differences emerge in subsequent measurement, income statement presentation, and the available exemptions.

|

Topic |

ASC 842 Operating |

ASC 842 Finance |

IFRS 16 |

|---|---|---|---|

|

Initial recognition |

ROU + Lease Liability |

ROU + Lease Liability |

ROU + Lease Liability |

|

Income statement |

Single lease expense |

Interest + Amortization |

Interest + Amortization |

|

ROU amortization |

Plug-balanced |

Straight-line |

Straight-line |

|

EBITDA impact |

Reduces EBITDA* |

Increases EBITDA* |

Increases EBITDA* |

|

Low-value exemption |

Not available |

Not available |

Available |

|

Short-term exemption |

Available (≤12 mo) |

Available (≤12 mo) |

Available (≤12 mo) |

* EBITDA impact: under an operating lease, the single lease expense sits above EBITDA and reduces it. Under finance lease (ASC 842) and IFRS 16 treatment, interest and amortization sit below EBITDA, so EBITDA is higher for the same lease. This is a presentation difference, not an economic one.

For a deeper comparison of how each standard affects financial reporting beyond the journal entries, see our guide on ASC 842 vs IFRS 16: Key Differences → /ifrs-16-vs-asc-842/

Stop calculating these entries by manually. Black Owl generates audit-ready ASC 842 and IFRS 16 journal entries automatically, posts them straight to your ERP (NetSuite, SAP, JD Edwards, QuickBooks), and produces a complete audit trail for every figure. Book a 10-minute demo →

Common Mistakes in Lease Journal Entries

After working through hundreds of implementations, the same errors show up repeatedly. None of them are careless – most happen because spreadsheets make certain things invisible until the auditor finds them.

1. Recording the full lease payment as expense

Under both ASC 842 finance leases and IFRS 16, the cash payment must be split into interest (income statement) and principal (balance sheet liability paydown). Booking the full payment as lease expense overstates EBIT and understates the liability balance.

2. Inconsistent IBR application

The IBR drives the entire valuation of the lease. Applying different IBR methodologies across leases – or worse, across different periods of the same lease – creates a comparability problem the auditor will flag. Document the IBR policy once and apply it consistently.

3. Missing modifications and remeasurements

Lease modifications (term extensions, scope changes, payment changes) require a remeasurement of the lease liability and a corresponding adjustment to the ROU asset. Many spreadsheet-based teams forget the remeasurement entry entirely, leaving the books carrying a stale liability balance.

4. Confusing operating vs finance classification

Under ASC 842, lessees must run the 5-criteria classification test at lease commencement. Misclassification flips the income-statement presentation entirely (single lease expense vs interest + amortization) and impacts EBITDA. When in doubt, document the classification analysis in writing – your auditor will ask.

How Software Automates These Entries

Calculating lease accounting journal entries manually for ten leases is tedious. For a hundred leases – with monthly entries, quarterly remeasurements, and an audit cycle layered on top it is functionally impossible to do without errors.

Black Owl handles the calculation, the entries, and the ERP posting automatically – with IBR documentation, modification history, and roll-forward schedules built into the audit trail. The entries shown in this article are generated in seconds from the lease contract data. No separate spreadsheet, no manual journals

- Calculates the ROU asset, lease liability, interest, and amortization at every period end.

- Generates compliant journal entries for ASC 842 (operating and finance), IFRS 16, and GASB 87 – and posts them automatically to your ERP.

- Maintains a complete audit trail with every assumption documented (IBR, classification rationale, modification history).

- Handles modifications, remeasurements, and terminations without spreadsheet acrobatics.

- Produces audit-ready reports and roll-forward schedules in one click.

See it in action: book a 10-minute demo and walk through how Black Owl auto-generates the same entries shown in this article – for your actual leases. No prep work required. →

Frequently Asked Questions

What is the journal entry for an operating lease under ASC 842?

At commencement, debit Right-of-Use Asset and credit Lease Liability for the present value of future lease payments. Each subsequent period, debit Lease Expense (the straight-line amount) and credit Cash for the payment, then plug-balance the ROU Asset and Lease Liability for amortization and interest so total lease expense remains straight-line.

How are finance lease journal entries different from operating lease entries?

Finance leases split the expense into Interest Expense and Amortization Expense, both recorded separately. Operating leases recognize a single, straight-line Lease Expense – even though the underlying ROU asset and lease liability still appear on the balance sheet. The income statement presentation is the most visible difference.

Are lease accounting journal entries the same under IFRS 16 and ASC 842?

Initial recognition is the same: debit ROU Asset, credit Lease Liability. The subsequent entries differ. IFRS 16 treats almost every lease like an ASC 842 finance lease – interest plus amortization, with no straight-line single-expense option. ASC 842 retains the operating-lease classification with the plug-balanced single expense.

How often are lease accounting entries recorded?

Typically monthly: one set of entries to record the lease payment, interest, and amortization. Lease modifications and reassessments require additional entries when those events occur. Year-end disclosures require roll-forward schedules from the cumulative monthly entries.

Can lease accounting software generate journal entries automatically?

Yes. Platforms like Black Owl Systems generate all required journal entries automatically from the lease contract data, post them to any ERP, and maintain a full audit trail with every assumption documented. This is the same workflow Big 4 auditors expect to see during fieldwork.

What is an ROU asset journal entry?

The ROU (right-of-use) asset journal entry records the lessee’s right to use the leased asset over the lease term. At commencement, ROU is debited for the present value of lease payments (plus any prepaid rent and initial direct costs, less lease incentives), and the lease liability is credited for the present value of future payments.

Bringing it all together

Lease accounting under ASC 842 and IFRS 16 turned a one-line rent expense into a portfolio of journal entries, schedules, and disclosures that get more complex with every modification and reassessment. The math is straightforward; the operational discipline of doing it right, every period, across the entire lease portfolio, is where teams lose hours and risk audit findings.

If your team is still running this in spreadsheets and you’re starting to feel the strain, the next step is short: see how Black Owl handles it for organizations with anywhere from 5 to 5,000 leases. The demo is 10 minutes and we use your actual lease data.

Related resources

- ASC 842 Lease Accounting: Complete Guide

- IFRS 16 vs ASC 842: Key Differences Explained Simply

- Right-of-Use Assets and Lease Liabilities Explained

- Incremental Borrowing Rate (IBR) for Lease Accounting

- Lease Amortization Schedule: Step-by-Step Guide

Want a working template to follow along? Download our free ASC 842 Journal Entries Excel template – pre-built formulas, sample data, and ROU/liability schedules included.

Greg Kautz

http://blackowlsystems.comGreg Kautz, CPA, CMA is a seasoned management consultant and professional accountant with over 40 years of experience in the consulting and energy sectors. At Black Owl Systems, Greg brings deep expertise in ERP systems, corporate finance, strategic planning, and technology integration.