Prepaid Rent Under ASC 842: Accounting Treatment, Journal Entries & Examples

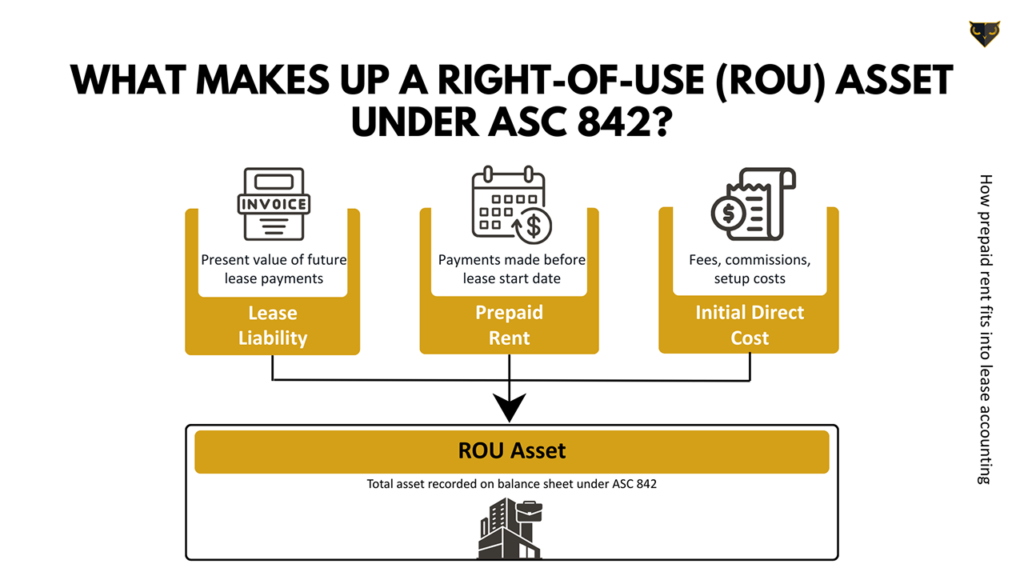

Under ASC 842, prepaid rent is no longer recorded as a separate asset on the balance sheet. Instead, it is folded into the right-of-use (ROU) asset at lease commencement, alongside the lease liability (the present value of future payments) and any initial direct costs incurred to obtain the lease. The lease liability itself is calculated separately based on future cash flows.

This guide explains how prepaid rent is accounted for under ASC 842, how it differs from deferred rent, the correct journal entries to record at commencement and throughout the lease, and a worked example with real numbers. A free Excel template is included at the end.

Quick definition: Prepaid rent is rent paid before the lease commencement date or in advance of the period it covers. Under ASC 842, prepaid rent increases the right-of-use asset but does not directly reduce the lease liability.

Key takeaways

- Prepaid rent is no longer a stand-alone balance sheet account under ASC 842 – it is rolled into the ROU asset.

- Prepaid rent increases the ROU asset value but does not reduce the lease liability.

- Prepaid rent is different from deferred rent: prepaid is cash paid in advance; deferred is the timing difference between cash and straight-line expense.

- Common mistake: maintaining a separate “Prepaid Rent” account in the GL alongside the ROU asset – leads to double counting.

- Lease accounting software handles prepaid rent automatically as part of ROU asset recognition.

What is Prepaid Rent?

Prepaid rent is any rent payment made before the period it covers. It can occur at lease commencement (a security-style payment for the first months) or anywhere along the lease term (when the tenant pays the next quarter or year up front to lock in terms or earn a discount).

Under the legacy ASC 840 standard, prepaid rent sat on the balance sheet as a separate asset account, typically labeled “Prepaid Rent.” The asset was reduced over time as the related rent expense was recognized. Simple, predictable, and decoupled from any other lease accounting concept.

ASC 842 changed this – and the change still trips up teams that have been doing lease accounting for years. Under the new standard, prepaid rent doesn’t get its own account. It becomes part of the ROU asset measurement at commencement.

Defining Prepaid Rent and Lease Payments

Lease payments under ASC 842 include all the cash the lessee will pay the lessor over the lease term, plus any cash already paid before commencement. The standard splits these payments into two streams for accounting purposes:

- Future lease payments – the basis for calculating the present value of the lease liability.

- Cash flows at or before commencement – including prepaid rent, initial direct costs (broker commissions), and any lease incentives received from the lessor (negative adjustment).

The first stream defines the lease liability. The second stream adjusts the ROU asset upward (prepaid rent and IDC) or downward (incentives). The two start at similar values but diverge from day one.

How Prepaid Rent is Accounted for Under ASC 842

Under ASC 842, prepaid rent is no longer recorded as a separate asset. Instead, it is included in the right-of-use (ROU) asset at lease commencement.

Here’s how it works:

- 1. Prepaid rent is paid before the lease start date.

- 2. The payment is included in the ROU asset calculation.

- 3. The lease liability is calculated separately based on future lease payments.

As a result, prepaid rent increases the ROU asset but does not directly reduce the lease liability.

Don’t book a separate “Prepaid Rent” GL account. Under ASC 842, prepaid rent lives inside the ROU asset balance. Maintaining a separate account is a common mistake that double-counts the prepayment and triggers audit questions.

Prepaid Rent vs Deferred Rent

These two concepts get confused constantly because they both involve timing differences in lease accounting. The distinction matters:

|

Concept |

Definition |

When It Arises |

Treatment Under ASC 842 |

|---|---|---|---|

|

Prepaid Rent |

Cash paid BEFORE the period it covers |

Lease commencement or early payment |

Folded into ROU asset |

|

Deferred Rent |

Timing difference between cash paid and straight-line expense |

Rent-free periods, escalating rent, step-ups |

Folded into ROU asset / lease liability calculation |

Both concepts no longer have their own ledger accounts under ASC 842. They are absorbed into the ROU asset and lease liability calculations. For the deeper deferred rent walkthrough, see our companion guide on Deferred Rent Entry Explained.

Worked Example: Prepaid Rent at Lease Commencement

Imagine your company signs a 5-year office lease with the following terms:

- Annual lease payment: $100,000, payable at the end of each year

- Lease term: 5 years

- Incremental borrowing rate (IBR): 5%

- Prepaid rent: $20,000 (paid at commencement to secure the lease)

- No initial direct costs, no lease incentives

Step 1 – Compute the lease liability:

PV of five $100,000 annual payments discounted at 5% = $432,948.

Step 2 – Compute the ROU asset:

- Lease liability: $432,948

- Plus prepaid rent: + $20,000

- ROU asset at commencement: $452,948

Initial journal entry

|

Account |

Debit |

Credit |

|

Right-of-Use Asset |

$452,948 |

|

|

Lease Liability |

$432,948 |

|

|

Cash (prepaid rent) |

$20,000 |

To record the ROU asset, lease liability, and prepaid rent at lease commencement under ASC 842.

Notice: there is no separate “Prepaid Rent” account. The $20,000 cash payment goes directly into the ROU asset balance, and the lease liability reflects only the present value of future cash payments.

Journal Entries Throughout the Lease

Once the prepaid rent is captured in the ROU asset at commencement, ongoing accounting treats the lease the same as any other lease under ASC 842 – operating or finance, depending on classification.

Year 1 – Operating lease treatment

Total lease cost over 5 years = $500,000 in scheduled payments + $20,000 prepaid = $520,000. Spread straight-line over 5 years = $104,000 per year of lease expense.

|

Account |

Debit |

Credit |

|

Lease Expense |

$104,000 |

|

|

Cash (annual payment) |

$100,000 |

|

|

Right-of-Use Asset (amortization) |

$4,000 |

Year 1 entry under ASC 842 operating lease treatment, including the prepaid rent component.

By the end of Year 5, the entire ROU asset balance (including the original prepaid rent component) has been amortized to zero, and the lease liability has been fully repaid.

Prepaid rent calculations for ASC 842 are easy to mishandle in spreadsheets – especially when prepaid amounts arrive mid-lease or get reset by modifications. Black Owl rolls them into the ROU asset automatically and adjusts every period without manual intervention. See how it works →

Common Mistakes with Prepaid Rent Under ASC 842

1. Maintaining a separate “Prepaid Rent” GL account

This is the most common error. Teams transitioning from ASC 840 keep the legacy account out of habit, then track the same balance inside the ROU asset – double counting the prepayment. The correct approach is to retire the standalone Prepaid Rent account at transition and let the ROU asset capture the balance.

2. Reducing the lease liability for prepaid rent

Prepaid rent does NOT reduce the lease liability. The lease liability is the present value of future payments. Prepaid amounts are already paid – they reduce cash and increase the ROU asset, never the liability.

3. Forgetting to update the ROU asset when prepaid rent is received mid-lease

If the lessee makes an additional prepayment after commencement (e.g., paying the next quarter early to secure a discount), the ROU asset must be increased by that amount. Many spreadsheet-based teams record only the cash movement and forget the ROU adjustment.

4. Confusing prepaid rent with deferred rent

Different concepts, different mechanics. Prepaid is cash paid early; deferred is a timing difference between cash payments and straight-line expense. Both are absorbed into the ROU asset under ASC 842 but for different reasons.

How Software Automates Prepaid Rent Accounting

Calculating prepaid rent treatment for one lease is straightforward. For a portfolio of dozens or hundreds of leases – with prepayments at commencement, mid-lease prepayments, modifications that reset terms, and multi-currency conversions – it becomes a spreadsheet maintenance nightmare.

Lease accounting software like Black Owl Systems handles the entire workflow:

- Captures prepaid rent at lease commencement and adds it to the ROU asset automatically.

- Handles mid-lease prepayments by remeasuring the ROU asset and updating the schedule.

- Maintains the audit trail showing how every cash movement flows into the ROU balance.

- Generates compliant journal entries and posts them directly to your ERP.

- Produces audit-ready disclosures with the prepaid rent component fully reconciled.

See it in action: book a 10-minute demo and walk through how Black Owl handles prepaid rent – for your actual leases.

Frequently Asked Questions

Is prepaid rent an asset under ASC 842?

Yes, but it is no longer a stand-alone asset. Prepaid rent is rolled into the ROU asset on the balance sheet at lease commencement, increasing the ROU value without affecting the lease liability.

How does prepaid rent affect the lease liability?

Prepaid rent does not reduce the lease liability directly. The lease liability is the present value of remaining future lease payments – and prepaid amounts are not future payments. They reduce cash and increase the ROU asset.

What is the difference between prepaid rent and deferred rent?

Prepaid rent is cash paid BEFORE the period it covers. Deferred rent is the timing difference between cash paid and the straight-line lease expense recognized over the term (common with rent-free periods or escalating payments). Under ASC 842, both concepts are folded into the ROU asset and lease liability.

How do you record prepaid rent in a journal entry under ASC 842?

At commencement, debit ROU Asset for the present value of payments PLUS the prepaid amount, credit Lease Liability for the PV of future payments only, and credit Cash for the prepaid amount actually paid. There is no separate Prepaid Rent account.

What happens to the legacy Prepaid Rent account at transition?

At ASC 842 adoption, any existing Prepaid Rent balance is reclassified into the ROU asset for the related lease. The standalone Prepaid Rent account is retired going forward, since prepaid amounts are now part of the ROU measurement.

Does Black Owl handle prepaid rent automatically?

Yes. Black Owl Systems incorporates prepaid rent into the ROU asset calculation automatically, generates the proper journal entries for ASC 842 compliance, and tracks the prepaid component in the audit trail without requiring a separate ledger account.

Bringing it all together

Prepaid rent treatment under ASC 842 isn’t complicated, but it does require unlearning the ASC 840 habit of maintaining a standalone Prepaid Rent account. Once the prepayment lives inside the ROU asset, the rest of the lease accounting workflow proceeds normally.

If your team is still maintaining separate Prepaid Rent accounts in spreadsheets, or if prepaid amounts are getting double-counted in your lease ledger, the next step is short: see how Black Owl handles prepaid rent automatically as part of the ROU asset. The demo is 10 minutes.

Related resources

Greg Kautz

http://blackowlsystems.comGreg Kautz, CPA, CMA is a seasoned management consultant and professional accountant with over 40 years of experience in the consulting and energy sectors. At Black Owl Systems, Greg brings deep expertise in ERP systems, corporate finance, strategic planning, and technology integration.