Straight-Line Depreciation: Formula and Example (2026)

Straight-line depreciation spreads the cost of an asset evenly across its useful life. The formula is (Cost − Salvage Value) ÷ Useful Life, and it is the simplest and most widely used depreciation method for office equipment, furniture, buildings, and many leased asset categories under ASC 842 and IFRS 16.

This guide explains the formula in plain English, walks through a worked example with real numbers, shows the journal entries you’ll need each year, compares straight-line to other depreciation methods, and clarifies when straight-line is the right choice. A free Excel calculator is included at the end.

Quick definition: Straight-line depreciation is a method of allocating the cost of a tangible fixed asset uniformly across its expected useful life. The result is a constant annual depreciation expense that simplifies financial reporting and tax planning.

Key takeaways

- Formula: Annual Depreciation = (Cost − Salvage Value) ÷ Useful Life.

- Use straight-line when an asset loses value evenly over time – office equipment, furniture, buildings, and most leased assets.

- The annual journal entry is always: Debit Depreciation Expense, Credit Accumulated Depreciation.

- Accelerated methods (declining balance, units of production) front-load depreciation; straight-line spreads it evenly.

- Software automates the calculation, journal entries, and disclosures across the entire fixed asset and lease portfolio.

What is Straight-Line Depreciation?

Depreciation is the accounting method used to allocate the cost of a tangible fixed asset over its useful life. It recognizes that the asset loses value as it is used, and matches that cost to the periods that benefit from its use – a core principle of accrual accounting known as the matching principle.

Straight-line is the simplest depreciation method. It assumes the asset loses an equal amount of value each year of its useful life, producing a constant annual depreciation expense. That predictability is why it dominates financial reporting: it is easy to calculate, easy to audit, and accurately reflects assets that lose value evenly over time.

Straight-Line Depreciation Formula

The formula has three inputs and one output:

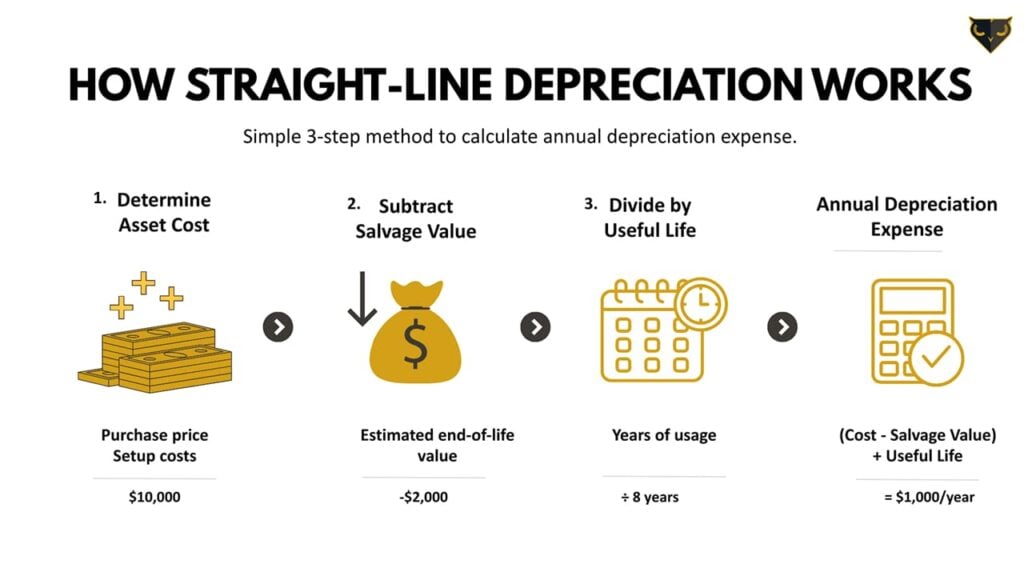

Annual Depreciation Expense = (Cost − Salvage Value) ÷ Useful Life

- Cost: the original purchase price of the asset, including setup, delivery, and installation costs.

- Salvage Value: the estimated value of the asset at the end of its useful life (also called residual or scrap value).

- Useful Life: the number of years the asset is expected to generate economic benefits.

The output – annual depreciation expense – is recognized each year for the entire useful life, until the book value of the asset equals its salvage value.

Straight-Line Depreciation Example

Suppose your company buys office equipment with the following terms:

- Purchase price: $10,000 (includes setup costs)

- Estimated salvage value: $2,000

- Useful life: 8 years

Apply the formula:

Annual Depreciation = ($10,000 − $2,000) ÷ 8 = $1,000 per year.

Each year for 8 years, the company records $1,000 in depreciation expense, until the book value of the asset reaches its salvage value of $2,000.

Year-by-year book value

|

Year |

Beginning Book Value |

Depreciation |

Ending Book Value |

|---|---|---|---|

|

1 |

$10,000 |

$1,000 |

$9,000 |

|

2 |

$9,000 |

$1,000 |

$8,000 |

|

3 |

$8,000 |

$1,000 |

$7,000 |

|

4 |

$7,000 |

$1,000 |

$6,000 |

|

5 |

$6,000 |

$1,000 |

$5,000 |

|

6 |

$5,000 |

$1,000 |

$4,000 |

|

7 |

$4,000 |

$1,000 |

$3,000 |

|

8 |

$3,000 |

$1,000 |

$2,000 |

Straight-Line Depreciation Journal Entry

The annual journal entry to record straight-line depreciation is the same every year for the entire useful life of the asset:

|

Account |

Debit |

Credit |

|

Depreciation Expense |

$1,000 |

|

|

Accumulated Depreciation |

$1,000 |

To record annual straight-line depreciation on office equipment ($10,000 cost, $2,000 salvage value, 8-year useful life).

A few mechanics worth understanding:

- Depreciation Expense is an income statement account that reduces net income.

- Accumulated Depreciation is a contra-asset account on the balance sheet that reduces the gross book value of the asset.

- The asset’s net book value at any time = Original Cost − Accumulated Depreciation.

- When the net book value equals the salvage value, depreciation stops.

Comparison with Other Depreciation Methods

Straight-line is the most common depreciation method, but it isn’t always the best fit. The three main alternatives:

Declining Balance (and Double-Declining Balance)

Front-loads depreciation. A higher percentage of the asset’s value is expensed in early years, with progressively less in later years. Best for assets that lose value rapidly when new (computers, vehicles).

Units of Production

Ties depreciation to actual usage rather than time. The annual expense varies year to year based on output (machine hours, miles driven, units produced). Best for manufacturing equipment whose wear depends on usage.

Sum-of-the-Years’ Digits

An accelerated method that allocates more depreciation in early years using a fraction based on remaining useful life. Less common today; still used in specific industry contexts.

|

Method |

Expense Pattern |

Best For |

|---|---|---|

|

Straight-Line |

Equal each year |

Buildings, furniture, most leased assets |

|

Declining Balance |

Front-loaded |

Vehicles, computers, technology |

|

Units of Production |

Varies by usage |

Manufacturing equipment |

|

Sum-of-the-Years’ Digits |

Front-loaded (smoother) |

Specific industry use cases |

Managing depreciation manually across a portfolio of fixed assets and leased assets quickly becomes a spreadsheet maintenance burden. Black Owl Systems automates depreciation schedules, journal entries, and disclosures alongside ROU asset amortization – in one unified platform. Book a 10-minute demo

When to Use Straight-Line Depreciation

Straight-line is the right choice in any of these situations:

- When asset usage is consistent over time

- For office equipment, furniture, and buildings

- When simplicity and predictability are priorities

- When compliance requires standardized reporting

- For ROU assets under ASC 842 finance leases and IFRS 16, which are amortized straight-line over the lease term

Avoid straight-line – and consider an accelerated method or units-of-production – when the asset clearly loses more value in early years (technology, vehicles) or when its wear is directly tied to output (manufacturing machinery).

Implications for Tax Purposes

Tax depreciation rules differ from financial reporting rules. In the United States, the IRS prescribes the Modified Accelerated Cost Recovery System (MACRS) for most tangible assets, which accelerates depreciation versus straight-line for tax purposes. Companies typically maintain two depreciation schedules – one for financial reporting (often straight-line) and one for tax (often MACRS) – and reconcile the difference through deferred tax accounting.

In Canada, the Capital Cost Allowance (CCA) system fills the same role, with prescribed rates by asset class. International standards (IFRS) generally permit straight-line and other methods, with the choice based on the consumption pattern of the asset’s economic benefits.

Stop maintaining separate depreciation schedules in spreadsheets. Black Owl handles fixed asset depreciation, lease amortization, and book vs tax reconciliation in one place. See how

Frequently Asked Questions

What is the formula for straight-line depreciation?

(Cost − Salvage Value) ÷ Useful Life. The result is the annual depreciation expense recorded each year until the book value of the asset equals its salvage value.

Why is straight-line depreciation the most common method?

It is the simplest to calculate, the easiest to audit, and accurately reflects assets that lose value evenly over time. It also simplifies tax compliance and financial reporting under standardized frameworks.

What is the difference between straight-line and accelerated depreciation?

Straight-line spreads cost evenly across the useful life. Accelerated methods (such as declining balance) front-load depreciation, recognizing more expense in early years and less in later years. Accelerated methods better match assets that lose value rapidly when new.

Does straight-line depreciation apply to leased assets under ASC 842?

Yes, in many cases. ROU assets under ASC 842 finance leases and under IFRS 16 are amortized straight-line over the shorter of the lease term or the asset’s useful life. Under ASC 842 operating leases, the ROU amortization is plug-balanced so that total lease expense is straight-line.

What is the journal entry for straight-line depreciation?

The annual entry is: Debit Depreciation Expense (income statement) and Credit Accumulated Depreciation (contra-asset on the balance sheet) for the calculated annual depreciation amount. The entry is repeated each year until the book value reaches the salvage value.

Can software automate straight-line depreciation?

Yes. Platforms like Black Owl Systems automate depreciation schedules, generate journal entries, post them to any ERP, and produce disclosures – across both fixed assets and ROU assets – in one platform.

Bringing it all together

Straight-line depreciation is the workhorse of fixed asset accounting and lease amortization. The formula is simple, the journal entries are repetitive, and the audit trail is straightforward – until you’re managing dozens of fixed assets and hundreds of leases with different start dates, useful lives, and modifications. That’s where the operational burden compounds and spreadsheet errors creep in.

If your team is still managing depreciation alongside lease accounting in spreadsheets, the next step is short: see how Black Owl unifies fixed asset depreciation and ROU asset amortization in one platform. The demo is 10 minutes.

Related resources

Greg Kautz

http://blackowlsystems.comGreg Kautz, CPA, CMA is a seasoned management consultant and professional accountant with over 40 years of experience in the consulting and energy sectors. At Black Owl Systems, Greg brings deep expertise in ERP systems, corporate finance, strategic planning, and technology integration.